Our Business

Aviation

Overview of Aviation

Driving growth and transformation with the industry’s leading business platform

In the Aviation segment, we provide services including aircraft leasing and financing, aircraft engine leasing and parts sales1, as well as Japanese operating leases2 to airlines and other companies across various countries and regions worldwide. As a unified Group, we provide a wide range of high value-added services throughout the entire life cycles of aircraft and aircraft engines, from their purchase to use and retirement.

- 1.Business to dismantle engines of aircraft that are near retirement, overhaul and repair them, and sell them as separate parts to maintenance companies and airlines

- 2.Operating leasing for aircraft, engines, ships, etc., for airlines and shipping companies. Sold to Japanese investors in the form of an investment or asset holding, etc. based on a partnership agreement

- Main business

- Aircraft leasing

- Aircraft engine leasing and parts sales (engine dismantling and parts sales)

- Japanese operating leases

- Brokerage of aircraft and aircraft engine sales, etc.

Strengths of aviation

- Comprehensive group-wide capabilities to solve customers' problems across the entire life stages of assets

- A high-quality portfolio with 76.1% of the fleet being new-generation aircraft and the majority being narrow-body aircraft

- Industry leadership as the top independent aircraft engine leasing company, providing one-stop services including parts sales

- A Group culture of challenging next-generation technology areas including SAF

- Risk management capabilities through group governance

Aviation Initiatives

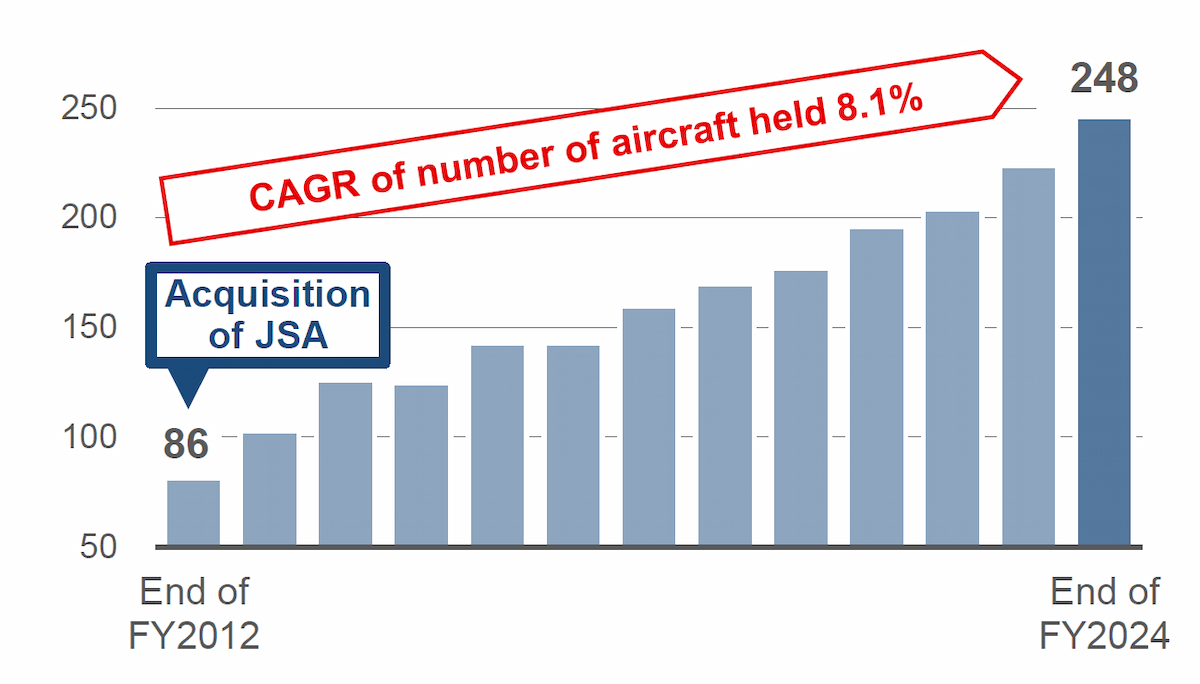

Main initiatives in the aircraft leasing business / Trend in the number of aircraft held

- Through our US subsidiary Jackson Square Aviation (JSA), we primarily engage in SLB1 transactions for new aircraft with global top-tier airlines. We are also expanding initiatives to lease the aircraft that JSA has directly ordered from manufacturers to airlines.

- We primarily provide long-term operating leases with terms of 10 to 12 years. In addition to stable revenues from long-term fixed leases, which form our profit base, we pursue an asset turnover model that generates gains by selling a portion of our owned aircraft.

- By maintaining a well-balanced approach to purchasing and selling primarily narrow-body aircraft, we have built a high-quality portfolio characterized by strong liquidity and a young average aircraft age.

- To support decarbonization, we are increasing the proportion of new aircraft with lower CO2 emissions—a ratio that ranks among the highest in the industry.

[Reference] As of the end of FY2024

| Average aircraft age | 5.1 years |

|---|---|

| Average remaining leasing term | 7.0 years |

| Percentage of narrow-body aircraft (based on book value) | 79.3% |

|---|---|

| Percentage of new generation aircraft (based on book value) | 76.0% |

- Since the acquisition of JSA, we have nearly tripled the number of aircraft held2 by continuing to purchase and sell aircraft (purchasing 20-30 and selling 10-15 annually).

- In 2025, a direct order was placed with Airbus for 50 new generation narrow-body aircraft.

- 1.Sales and lease back: A method of acquiring aircraft in which aircraft are purchased from customer airlines and then leased back to them.

- 2.The number of aircraft held after FY2021 includes the number of aircraft managed

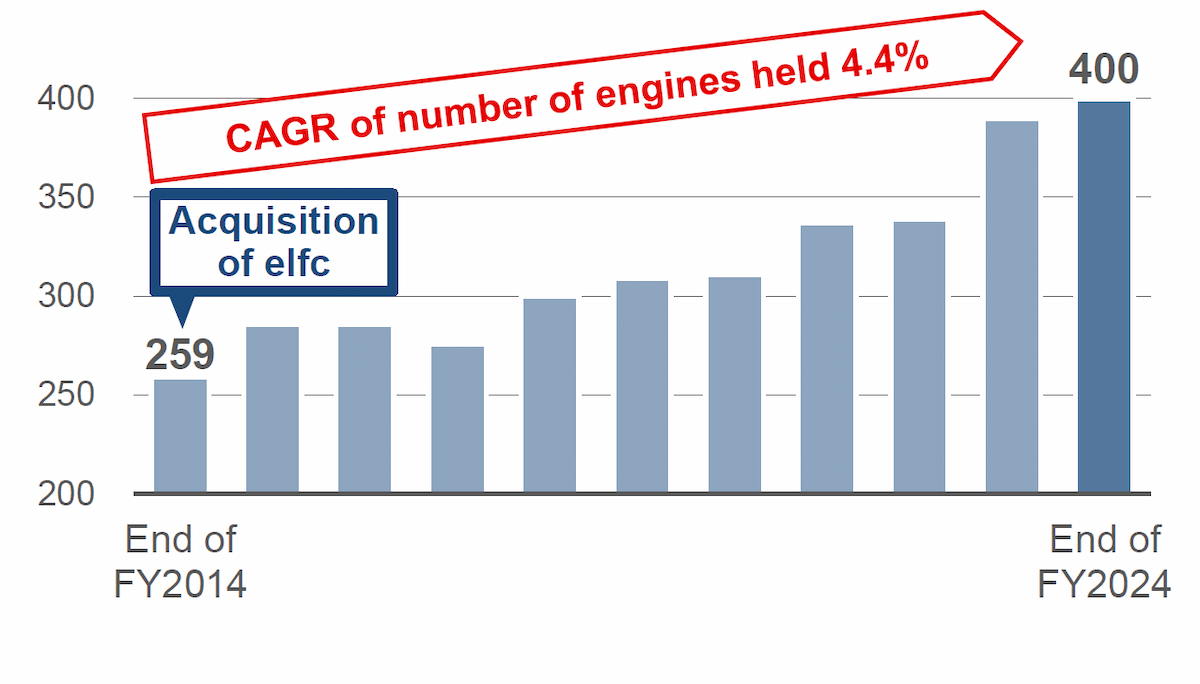

Main initiatives in the aircraft engine leasing business / Trend in number of engines held

- Through Engine Lease Finance (elfc), an Irish subsidiary which is the leading independent aircraft engine leasing company, we are engaging in spare engine leasing transactions with global airlines and engine maintenance companies.

- In addition to long-term leases of approx. 8 to 12 years, we also accommodate short-term contracts of less than one year. Our focus is on operating leases, and we generate gains not only from leasing revenue but also from engine sales and maintenance services.

- Similar to aircraft, we focus on building a portfolio of engines compatible with narrow-body aircraft, which offer high liquidity. Currently, we are working closely with engine manufacturers to promote the adoption of fuel-efficient engines for next-generation aircraft.

- INAV (a wholly-owned subsidiary of elfc, based in the US) is operating aircraft engine parts sales business, effectively creating synergies with elfc.

- We have increased the number of engines held* primarily through SLB transactions for newly manufactured engines.

- In 2025, a direct order was placed with CFM for 50 new generation engines

- *The number of aircraft engines held after FY2021 does not include the number of engines to be sold to inav.

Main initiatives in Japanese operating leases

- We originate and sell Japanese operating leases covering aircraft, aircraft engines, and other assets.

- We provide products to over 1,300 investors in Japan by leveraging the Mitsubishi Group’s network. In 2024, we established a domestic subsidiary* to further enhance our services.

- *MHC Aviation Services Co., Ltd.

Main initiatives toward decarbonization in the aviation domain

- We are focused on increasing the proportion of new, fuel-efficient aircraft and engines in our portfolio. In 2025, we are placing significant direct orders with manufacturers for next-generation aircraft and engines.

- We have invested in SAFFA Fund I, LP (SAFFA) to contribute to expanding the production of sustainable aviation fuel (SAF), which is expected to play a key role in decarbonizing the aviation industry.

SAFFA is a fund that aims to increase the supply of SAF by investing in and providing funds to SAF manufacturers, etc. Our Group is promoting decarbonization of the aviation industry through these investments.

In addition, we sowed seeds for transformation, such as signing partnership agreements with our investee partner companies to consider new businesses and considering commercializing businesses in next-generation technologies including SAF and electrification.

[Reference] Aviation business environment (forecast of global demand for commercial aircraft (number of aircraft))

- In 2025, global air passenger demand increased by around 10% from pre-COVID-19 levels.

Demand is forecasted to grow at an average annual rate of over 3% from 2025 through 2044 in line with GDP and population growth*. - Driven by the increase in air passenger demand, the demand for aircraft is expected to continue expanding.

The global aircraft fleet is projected to roughly double over the next 20 years.

- *“Quarterly Air Transport Chartbook Q1 2025” by International Air Transport Association (IATA), “Worldwide Market Forecast (2025-2044)” by Japan Aircraft Development Corporation.